Understanding Level Term Life Insurance & How it Works

Level term life insurance, also known as level benefit term life insurance, offers coverage for a fixed period, typically spanning 10 to 30 years. The term “level” indicates that both the premium payments and the death benefit stay unchanged throughout the policy period. This consistency makes financial planning and budgeting easier, making it an attractive choice for individuals seeking simple and dependable coverage.

How does this type of insurance work?

Level term life insurance is straightforward: you pay a consistent premium for a predetermined death benefit that remains unchanged for the entire policy term. This fixed premium simplifies budgeting for your insurance over time.

If you pass away within the policy term, your beneficiaries receive a predetermined lump sum, aiding them in covering immediate expenses and sustaining their lifestyle without financial strain, with the assurance of guaranteed support.

Level term life insurance also offers flexibility in coverage duration. You can choose a term that fits your financial obligations and life stage, whether it’s paying off a mortgage, supporting children through college, or planning for retirement. At the end of the term, you have the option to renew the policy, convert it to a permanent policy, or let it expire, based on your evolving needs.

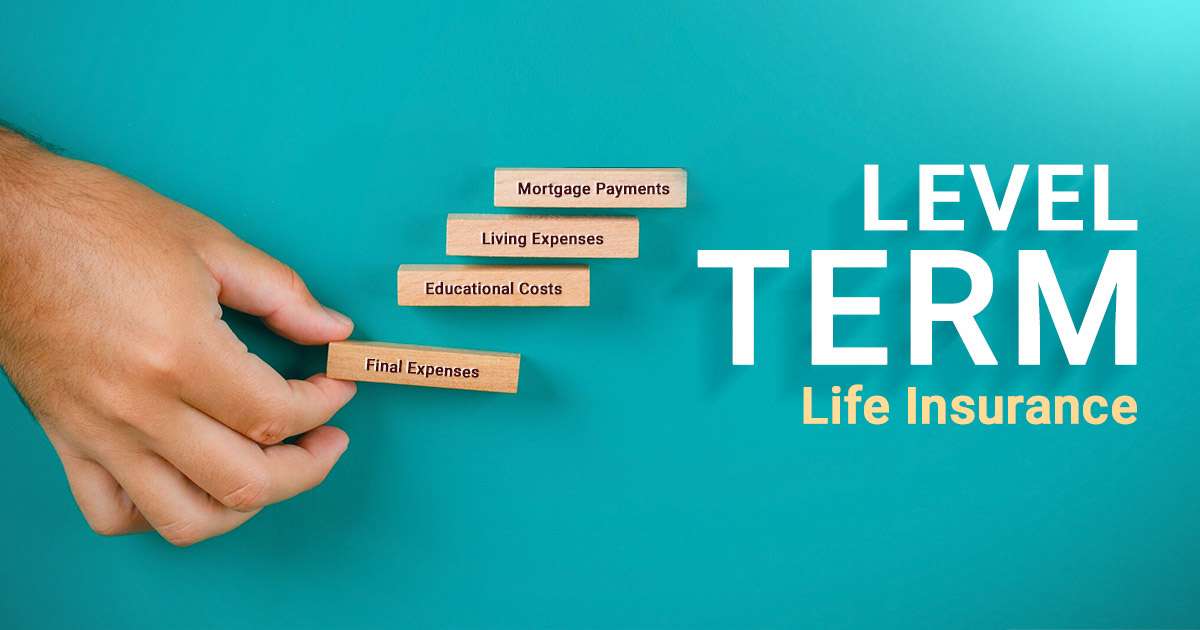

What kind of coverage does it provide?

Level term life insurance provides essential coverage to protect your loved ones’ financial well-being if you pass away unexpectedly. The death benefit given to your loved ones can help them manage different financial responsibilities, securing their continual financial well-being. Here are some common expenses that level term life insurance can help with:

- Mortgage Payments: If you have a mortgage or other outstanding debts, the death benefit can pay off these obligations, allowing your family to stay in their home without the burden of monthly payments.

- Living Expenses: The death benefit can help with daily living expenses like utility bills, groceries, and transportation costs, allowing your family to maintain their standard of living.

- Educational Costs: For families with children, level term life insurance can fund educational expenses, including tuition, books, and school supplies, securing their future and access to quality education.

- Final Expenses: This insurance can also pay for funeral and burial expenses, easing the financial burden of end-of-life arrangements for your loved ones.

What are the downsides to this type of insurance?

Before deciding, it’s important to grasp the drawbacks of level term life insurance, despite its advantages.

- Expiration of Coverage: Coverage expires at the end of the term. If you outlive the policy, you won’t receive any benefits unless you renew it, purchase a new one, or convert it into a permanent one. If you require coverage beyond the initial term, you might encounter higher premiums or fewer options, particularly if your health has worsened.

- Locked-In Rates: Rates are locked in, which may become disadvantageous if your health improves during the policy term. Since premiums are based on your health status at the time of application, any positive changes in your health won’t lower your premiums. You might find yourself paying an excess amount for coverage, particularly if you could be eligible for reduced rates due to improved health.

- Limited Flexibility: Fixed premiums and a predetermined death benefit provide stability and predictability. However, this lack of flexibility may not suit everyone’s needs, particularly if your financial situation or coverage requirements change over time. Level term policies, unlike whole life or universal life insurance, lack cash value and investment features, limiting long-term planning.

How does it compare to other insurance?

When comparing level term life insurance to other types, several factors differentiate them in terms of cost, coverage duration, and complexity.

- Affordability: Level term life insurance typically costs less than permanent policies like whole or universal life insurance due to temporary coverage.

- Coverage Duration: Level term life insurance provides coverage for a specific term, typically ranging from 10 to 30 years. This temporary nature of coverage makes it suitable for addressing short-term financial needs, such as paying off a mortgage or providing income replacement during your working years. Permanent life insurance provides coverage throughout your lifetime, unlike term insurance with a specific duration.

- Simplicity of Structure: Level term life insurance is known for its simplicity. It offers fixed premiums and a straightforward death benefit without the complexity of cash value accumulation or investment components. This simplicity makes it easier to understand and manage, especially for those prioritizing budget-friendly coverage without additional features.

Do you need level term life insurance?

Deciding if level term life insurance is suitable requires evaluating your finances, goals, and risk tolerance. Consider the following factors:

- Financial Responsibilities: Evaluate your financial obligations and consider how your loved ones would manage without your income. Level term life insurance can provide essential financial protection during specific periods, such as while paying off a mortgage, covering educational expenses for children, or supporting a spouse/partner. It could fit if you have time-limited financial obligations, like until kids are independent or a mortgage is paid.

- Budget Constraints: Consider your budget and whether you can afford the premiums associated with level term life insurance. Level term policies, lacking cash value accumulation, are typically cheaper than permanent life insurance options. If you’re looking for cost-effective coverage within your budget, level term life insurance may be a practical choice.

- Risk Management: Assess your risk tolerance and determine how much financial risk you will assume. Level term life insurance provides a predetermined death benefit for a specific term, offering stability and predictability. If you prefer a straightforward insurance solution without the complexities of investment features or cash value accumulation, level term insurance may be the right fit.

- Long-Term Financial Goals: Consider your long-term financial goals and whether level term life insurance aligns with them. If you require lifelong coverage or wish to build cash value over time, you may need to explore permanent life insurance options, such as whole life or universal life insurance. These policies offer coverage for your entire life and include investment components that can grow over time, providing additional financial security and flexibility.

Level term insurance is a good option

Level term life insurance offers simplicity, affordability, and reliable financial protection for a period. With fixed premiums and a predetermined death benefit, it provides peace of mind and helps you plan for the future. While it may not be the best fit for every one, level term life insurance serves as a valuable tool for individuals seeking basic yet essential coverage for their loved ones.